League of Legends Pro Gamer 'Ruler' Park Jae-hyuk Faces Tax Evasion Controversy Including Stock Name Trust

롤 프로게이머 ‘룰러’ 박재혁, 주식 명의신탁 등 탈세 논란

2026.03.31 12:20 UTC+9

AI Summary

Gen.G's Ruler faces tax evasion allegations regarding asset management. The Tax Tribunal dismissed his appeal, citing intentional tax avoidance. Riot Games Korea and KeSPA are currently reviewing the case for potential sanctions.

Park 'Ruler' Jae-hyuk, the Gen.G bot laner known for his stellar international performances and LCK titles, finds himself in hot water over tax evasion allegations. With the LCK season set to kick off on April 1, all eyes are on how both the league and the team will handle this situation.

The scandal broke on the 26th via a precedent found in the National Tax Legal Information System. While the documents initially masked the identity of the pro gamer, the details left little doubt it was Gen.G's own Ruler. The records suggest that beyond issues concerning labor costs from 2018 to 2021, there were further discrepancies in his 2023 comprehensive income tax filing, specifically regarding income disguised through borrowed-name stocks. Park's side appealed to the Tax Tribunal, claiming the authorities were being overly harsh, but the appeal was dismissed due to a lack of supporting evidence.

The crux of the matter lies in financial transactions between Park and his father. Park’s camp argued that payments were made to his father for serving as a de facto manager—a necessity, they claim, to handle the taxing schedule and health concerns since his debut as a minor. The tax authorities, however, disagreed. They pointed out that in the professional gaming ecosystem, the team manages almost everything—from bootcamp living to tournament participation, training, broadcasts, and advertisements—leaving little room for a separate personal manager.

The Tax Tribunal sided with the authorities. They noted that Park already had a separate agency handling contract negotiations and key business affairs. They also pointed out that his father rarely accompanied him to major overseas tournaments, and the services he allegedly provided didn't really exceed what any supportive parent might offer.

The issue of stock ownership by proxy was another major sticking point. While Park’s side insisted his father was merely managing assets with no intent to dodge taxes, tax authorities invoked Article 45-2 of the Inheritance and Gift Tax Act, which treats assets held under a different name as a gift. The burden of proof lies with the taxpayer to demonstrate no intent to evade tax, and it seems Park's team failed to clear that bar.

Authorities noted that Park could have easily managed his own investments. Instead, using his father's name meant dividend income and capital gains weren't attributed to him, but rather reported as his father's income—which was then used to cover his father's personal expenses or tax bills. This was not just a simple tax-saving measure; it was judged as a calculated move to dodge both comprehensive taxation and gift taxes on a significant scale.

The Tax Tribunal ultimately ruled that there was insufficient objective evidence to suggest a lack of intent to evade taxes. They specifically highlighted the repeated reporting of dividend income under the father's name as a clear red flag. The ruling explicitly states, 'This trust of property by name was carried out for the purpose of tax evasion,' leading to the dismissal of Park's appeal.

In the wake of the news, his agency, 'Supergent', stated on Instagram that this was simply an 'administrative oversight during asset management.' They claimed there was no real intent to gift assets, that the gift tax has since been paid in full, and that all assets have been returned to the player's name. Riot Games Korea commented that they are currently 'looking into the facts and reviewing the matter internally.'

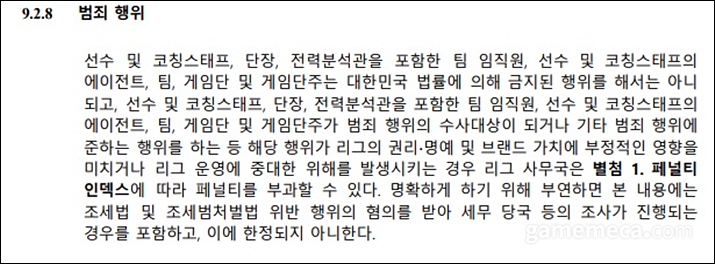

According to the 2026 LCK rulebook, Chapter 9, players and team staff are strictly forbidden from engaging in acts prohibited by South Korean law. If a player becomes the subject of a criminal investigation, the league can impose sanctions based on its 'Penalty Index.' This explicitly includes investigations into tax law violations, and the league notes that repeated or intentional offenses can result in the most severe penalties.

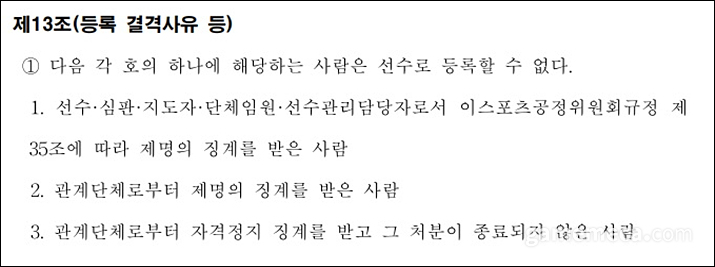

Furthermore, the Korea e-Sports Association (KeSPA) states that anyone under disciplinary action from related organizations is ineligible for registration. As these regulations also cover actions that damage the dignity of a professional athlete, the industry is waiting to see if further action will be taken beyond just the team and the league.

국가대표 출전 및 세계 대회 수상, LCK 리그 우승 등 뛰어난 성적으로 주목을 받아온 젠지 소속 원거리 딜러 선수 ‘룰러’ 박재혁에게 탈세 논란이 발생했다. 이번 사태는 오는 4월 1일 리그 개막을 앞둔 상황에서 불거진 것으로, 리그 및 팀 차원의 대응에 관심이 쏠리고 있다.

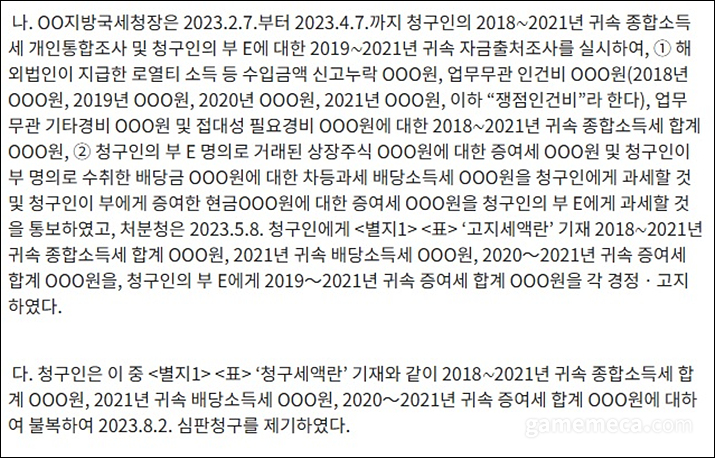

이번 사태는 지난 26일, 국세법령정보시스템에 등록된 판례를 통해 확인됐다. 해당 판례에서는 익명의 프로게이머로 처리되었으나, 문서에 등장하는 이력 등을 종합한 결과 젠지 소속 원거리 딜러 ‘룰러’ 박재혁 선수로 확인됐다. 문서에 따르면 2018년부터 2021년까지의 쟁점 인건비 문제에 더해, 한 차례 경정고지 이후에도 2023년 종합소득세 신고 과정에서 차명주식 관련 소득을 위장 신고한 정황이 드러났다. 당시 박 선수 측은 국세청의 처분이 과도하다고 주장하며 조세심판원에 심판을 청구했으나, 증빙 부족 등을 이유로 기각됐다.

사건의 핵심은 박 선수와 아버지 간의 금전 거래에 있다. 박 선수 측은 아버지에게 인건비를 지급했고, 아버지가 실질적인 매니저 역할을 수행했다고 주장했다. 미성년자 시절 데뷔 이후 과중한 일정과 건강 문제 등을 지원하기 위한 조치였다는 설명이다. 반면 과세당국은 프로게이머의 활동 구조를 근거로, 구단 계약 아래 이루어지는 합숙생활과 대회 참가, 훈련, 방송, 광고 등의 일정 대부분을 구단이 관리하고 있어 별도의 매니저 필요성이 낮다고 반박했다.

조세심판원 역시 이 같은 구조를 인정했다. 특히 아버지 외에도 별도의 에이전시와 매니지먼트 계약이 체결되어 있었고, 실제 계약 협상 등 주요 업무 역시 해당 에이전시가 담당한 점을 중요하게 봤다. 또한 아버지가 주요 해외 대회에 동행하지 않은 점, 수행했다고 주장한 업무가 부모가 통상적으로 제공할 수 있는 지원 범위를 크게 벗어나지 않는다는 점 등을 근거로 들었다.

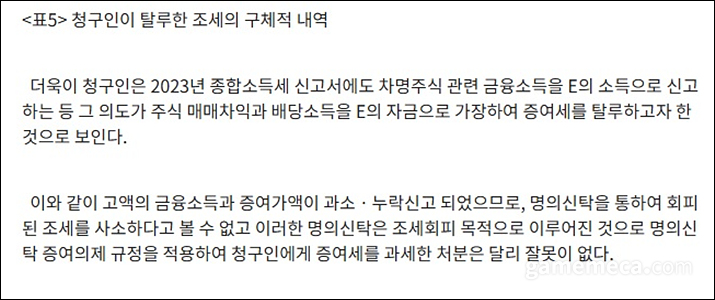

더불어 주식 명의신탁 문제도 주요 쟁점으로 지적됐다. 박 선수 측은 아버지가 단순히 자산을 관리했을 뿐 조세회피 목적은 없었다고 주장했지만, 과세당국은 상속세 및 증여세법 제45조의2에 따라 재산의 실질 소유자와 명의자가 다른 경우 원칙적으로 증여로 간주된다고 밝혔다. 이 경우 조세회피 목적이 있는 것으로 추정되며, 이를 반박할 책임은 납세자에게 있으나 박 선수 측은 이를 충분히 입증하지 못한 것으로 판단됐다.

특히 박 선수 본인 명의로도 충분히 투자 및 자산 관리가 가능했음에도 아버지 명의를 사용한 점, 그로 인해 발생한 배당소득과 매매차익이 선수 본인에게 귀속되지 않고 아버지의 소득으로 신고된 점, 그리고 해당 자금이 아버지의 세금 납부나 개인 지출에 사용된 점 등이 문제로 지적됐다. 이 과정에서 종합과세 대상인 배당소득과 증여세가 동시에 회피된 것으로 보이며, 그 규모 역시 단순한 절세 수준을 넘어선 것으로 판단됐다.

조세심판원은 이러한 사실관계를 받아들여 조세회피 목적이 없었다는 점에 대한 객관적이고 충분한 증빙이 부족하다고 봤다. 특히 배당소득을 반복적으로 아버지의 소득으로 신고한 행위는 단순한 자산 관리 목적을 넘어선 것으로 해석됐다. 판결문에서도 “이러한 명의신탁은 조세회피 목적으로 이루어진 것”이라고 명시하며 박 선수 측의 심판청구를 기각했다.

에이전시 ‘수퍼전트’ 측은 해당 문제가 가시화된 이후 공식 인스타그램을 통해 “이번 사안은 자산 관리 과정에서 발생한 행정적 미숙으로 인한 세금 부과 건”이라고 밝혔다. 또한 “실질적인 증여 의도는 없었으나 명의신탁으로 인해 증여세가 발생했으며, 해당 세금은 이미 전액 납부를 완료했다. 관련 자산 역시 선수 본인 명의로 모두 환원된 상태”라고 설명했다. LCK를 주관하는 라이엇코리아 측에서는 “내부적으로 사실 관계 파악 및 검토 중이다”라며 입장을 밝혔다.

한편, LCK 사무국이 공개한 2026년 공식 규정집 제9장에 따르면 선수와 팀 임직원, 에이전트, 게임단 및 관계자는 대한민국 법률에 의해 금지된 행위를 해서는 안 된다. 만약 수사 대상이 되거나 범죄 행위에 준하는 사안이 발생할 경우, 리그 사무국은 페널티 인덱스에 따라 제재를 부과할 수 있다. 여기에는 조세법 및 조세범처벌법 위반 혐의로 세무당국의 조사가 진행되는 경우도 포함되며, 반복적이고 고의적인 위반일 경우 최고 수준의 페널티가 적용될 수 있다고 명시되어 있다.

더불어 한국e스포츠협회(KeSPA) 또한 경기인 등록 결격사유로 관계단체로부터 자격정지 징계를 받고 그 처분이 종료되지 않은 사람은 선수로 등록할 수 없다고 명시했다. 더불어 징계 사유 및 대상에 스포츠인으로서의 품위를 훼손하는 경우가 포함된 만큼, 팀 및 리그 외에도 관련 단체에서의 조치에도 귀추가 주목되는 상황이다.

This news was translated by AI.

I am dedicated to games and writing. viina@gamemeca.com

READ MORE

-

The Sorrows of an Office Worker 'Chubby Cheeks'? Trickcal: Fatima Unveiled

The Sorrows of an Office Worker 'Chubby Cheeks'? Trickcal: Fatima Unveiled

-

FC Online '2026 FSL Summer' Kicks Off in July with Google Play

FC Online '2026 FSL Summer' Kicks Off in July with Google Play

-

Granblue Fantasy Versus: Rising, Version 2.60 Update Arrives September 17

Granblue Fantasy Versus: Rising, Version 2.60 Update Arrives September 17

-

Martial Artist Raider, Virtua Fighter CROSSROAD 'Bakunawa Killer' Revealed

Martial Artist Raider, Virtua Fighter CROSSROAD 'Bakunawa Killer' Revealed

-

[Hidden Gems] "The cat made a mess" Steam 'Very Positive' room cleaning game 'Cozy Cleaner'

[Hidden Gems] "The cat made a mess" Steam 'Very Positive' room cleaning game 'Cozy Cleaner'

-

SNK Announces Remaster of ART OF FIGHTING Gaiden R, Teasing King and Yuri

SNK Announces Remaster of ART OF FIGHTING Gaiden R, Teasing King and Yuri

-

Motel PC cafes are illegal, MCST and GRAC to strengthen crackdown on 'Gametels'

Motel PC cafes are illegal, MCST and GRAC to strengthen crackdown on 'Gametels'

-

Explosive Popularity on Mobile, Pokemon Champions Hits 10 Million Downloads

Explosive Popularity on Mobile, Pokemon Champions Hits 10 Million Downloads

MOST POPULAR NEWS

- "Requested game blocking to credit card companies": Even threats have emerged

- Mabinogi Eternity, Rebuilt with Unreal Engine 5, to Begin Testing This Autumn

- Revamped Lobby, Nexon Shares Direction for KartRider Revival Project

- Monster Hunter meets Animal Crossing? New action game 'Monster Fantasy' revealed

- 90s Magical Girl Nostalgia: Astraea Oratio Character Reveal

- Valve reveals Steam Machine pricing, starting at 1.61 million KRW

- An Entire Fantasy RPG Packed In: Neverness to Everness Version 1.2 Promises Massive Content

- Zero Tolerance Policy: Nexon Announces Investigation Request for 'Mabinogi Mobile' Leaks

- Type-Moon's 'Tsukihime -A piece of blue glass moon-' Remake Korean Version to Launch on August 13

- Faker's 6th Championship Captured: T1 2025 Worlds Skin Revealed

MEDIA PARTNERSHIPS

GAMEMECA SNS